Can Neobanks Succeed in India?

Just before the COVID-19 pandemic truly hit start-up deal activity, the US banking start-up Chime closed its Series E round of funding. The $700M deal led by DST Global valued the company at a whopping $6B post-money. Chime is one of a handful of American and European neobanks - digital only banks - that is aiming to change the way retail banking happens. There are a number of factors that have led to the rise of neobanks over the last half decade. These include legacy tech infrastructure that doesn't appeal to mobile-first millennials, broadly poor customer service, including charging high overdraft fees and providing unattractive interest rates, which only further alienates a poorly served customer base, and in the case of the EU, a proactive regulatory environment that aimed to foster competition. There's been a fair bit of buzz about neobanks in India recently, so this article is an attempt to lay out a bit of background about neobanks in the US and EU and think about what their Indian equivalents might look like.

Neobanks operating in the US and EU

Neobanks in the EU and the US

In some ways, the rise of retail neobanks really started in Europe - home to players like N26, Revolut, Monzo, and Starling. Post 2008, European regulators worked to create more competition in the banking industry, making it easier for neobanks to get a license, and gain real traction. For example, UK neobanks have ~20M customers (roughly a third of the country's population).

In the US, the financial landscape is different, and more challenging. The regulatory landscape is complex with decision-making authority split cross multiple agencies, making applying for and getting a bank license a truly difficult, and costly, endeavor. As a result, US neobanks work with FDIC insured partner banks (quite often regional banks lacking cutting-edge tech capabilities, for whom the neobank acts as a good lead generation tool), and banking-as-a-service partners, to offer bank accounts and other features (debit cards, ACH, etc.). Neobanks use tech to better serve their customers. By offering not just a great user experience, but also features like personal finance management, automatic savings, early paycheck access, no overdraft fees, etc. they have been able to create a customer base of brand conscious, and poorly served millennials.

In The Ascent of Money, Niall Ferguson writes: "In finance, small is seldom beautiful." The neobanks are turning this sentiment on its head, starting with one niche product with which they hope to gain traction, and then expand. The challenge, especially in the US, is an inefficient cost structure, with partners taking a significant chunk of revenue. Not being a fully regulated bank also means things like credit, and joint accounts are off the table. Monetization for these start-ups is largely through the following avenues:

Interest income on liquid assets,

Subscription fees (more relevant in Europe where a 'freemium' model is common), and

Interchange fees. The most important monetization mechanism at present. The interchange fees in the US continues to be rich (especially on credit cards, but even on debit cards, especially compared to the EU). If a neobank can become a customer's primary bank account with a linked Visa or MasterCard, that's a good source of revenue.

Clearly, though, these are just a starting point, and the revenue models of most neobanks are still far from proven.

Nascent neobanks in India

Neobanks seem to be the flavor of the season with VCs in India. Note this February article in Mint: "Neo banks raised $116 million in 2019, up seven times year-on-year. While the figure is not huge, what’s striking is that many of these firms have raised seed rounds of $5-20 mn on paper ideas alone."

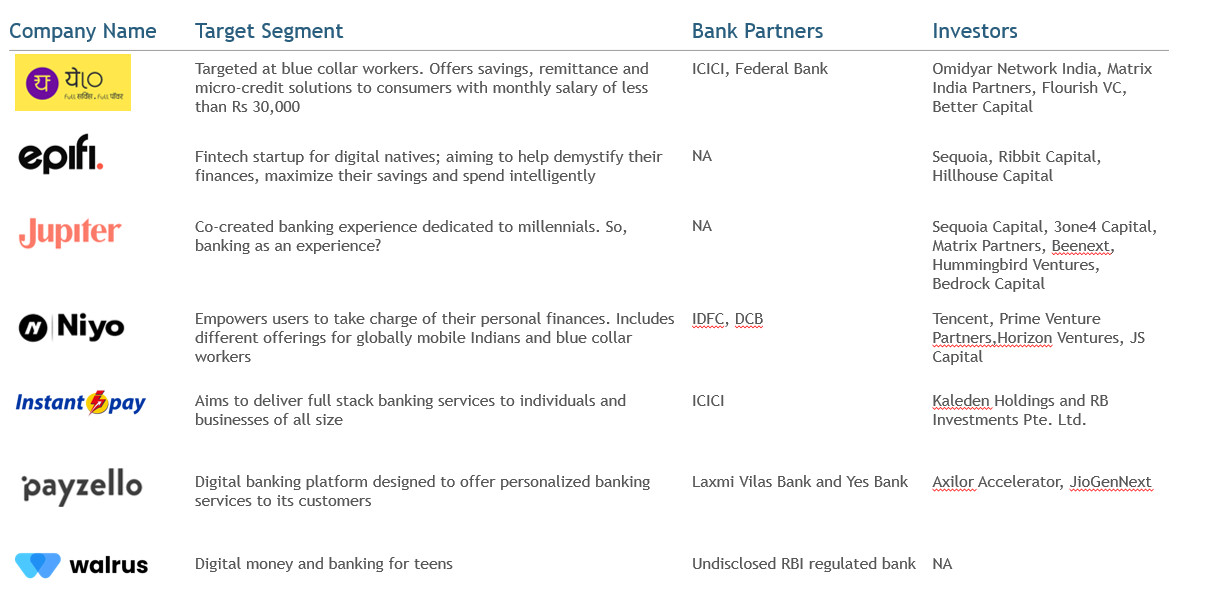

Neobanks are still quite a nascent idea in the Indian context, each trying to target a slightly different segment, and solve a slightly different problem. I have collated the details I could find on some of the big name start-ups in the space below.

Source: Company websites

India startups often suffer from copycat syndrome, wherein an idea that has taken off in Silicon Valley is adapted to the Indian context. This is not to say that there isn't virtue in adapting new business models to a local context, but it's worth taking a pause to recap what India's digital financial landscape looks like, and where these start-ups can potentially play.

The banking landscape in India

Retail banks, classified as Scheduled Commercial Banks, are regulated by the Reserve Bank of India. The subsets within this broad categorization include public sector banks, private sector banks, regional rural banks, payments banks, and small finance banks.

Between 1969 - 1980, the Indian state carried out two rounds of nationalization (14 banks in 1969, and a subsequent 4 in 1980) that meant it controlled ~90% of the banking industry. Post liberalization, the RBI began licensing a new wave of private banks. Some of the now familiar names in Indian banking - IndusInd, Axis , ICICI, HDFC, Yes Bank - were created during the 1993 - 2003 period.

In 2013, the RBI constituted the Nachiket Mor committee to study and propose ways to further financial inclusion, and increase access to financial services. On the recommendations of the committee, it introduced licenses for two kinds of niche banks:

Payments Banks: to provide small savings accounts, and payments and domestic remittance services via a low-cost, high-technology model (and to provide a broader regulatory framework for the then burgeoning mobile wallet or pre-paid instrument providers to expand their operations)

Small Finance Banks: to provide savings vehicles, and supply of credit to small business units, small and marginal farmers, micro and small industries, and other unorganized sector entities

In 2015, the RBI gave 11 entities licenses to operate as payments banks (including PayTM, and telco players like Airtel, Reliance, and Vodafone). However, this category of bank has not taken off - only 7 of the 11 entities even started operations, and of those only 4 have any sort of fully fledged business. There were certain constraints in the RBI's regulations that hobbled payments banks from the start. These included:

Restrictions of maximum balance of Rs 1,00,000 per customer

At least 75% statutory liquidity ratio (vs 22% for other commercial banks)

Inability to provide loans or credit cards

That the experiment in payments banks has failed is something that even the RBI seems to have realized. It announced last year that payments banks can apply for conversion into small finance banks, which have had much more success, given their looser regulatory requirements, and ability to lend.

The failure of the payments bank model, probably also has a lot to a whole host of things that have changed in India's financial landscape since 2014. For one, the country has made massive strides in financial inclusion as a result of the Pradhan Mantri Jan Dhan Yojana initiative, which was launched in late 2014, and largely driven by public sector banks. The figures below speak for themselves.

Source: BIS Papers No. 106, The design of digital financial infrastructure: lessons from India

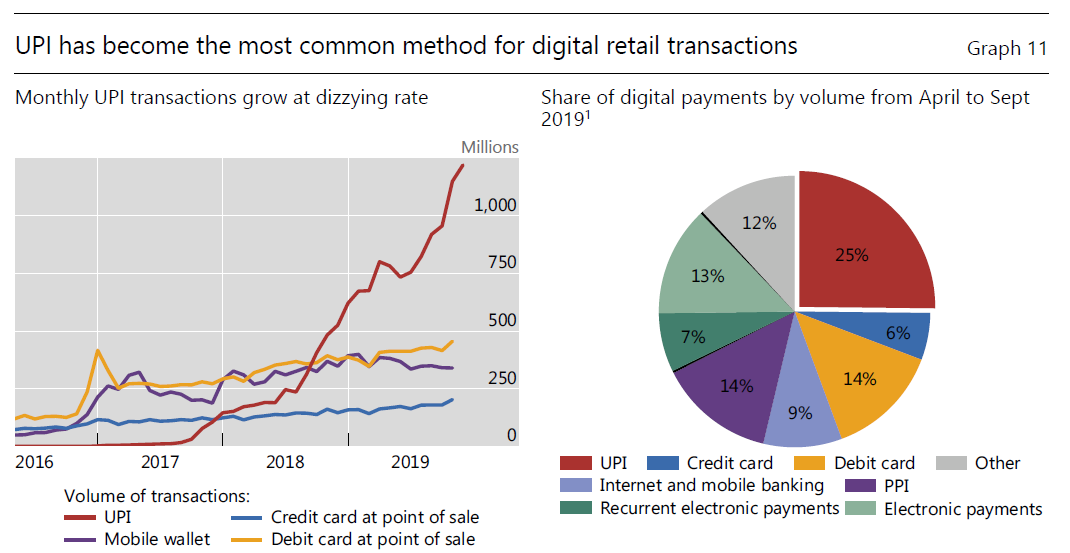

Then, of course, in 2016 came the launch of the Unified Payments Interface (UPI), the instant, real-time, and interoperable payment system developed by the National Payments Corporation of India (NPCI), which has far outstripped any other form of digital retail transaction in the country. (Just look at the interaction of UPI and mobile wallets trend lines in the graph below!)

Source: BIS Papers No. 106, The design of digital financial infrastructure: lessons from India

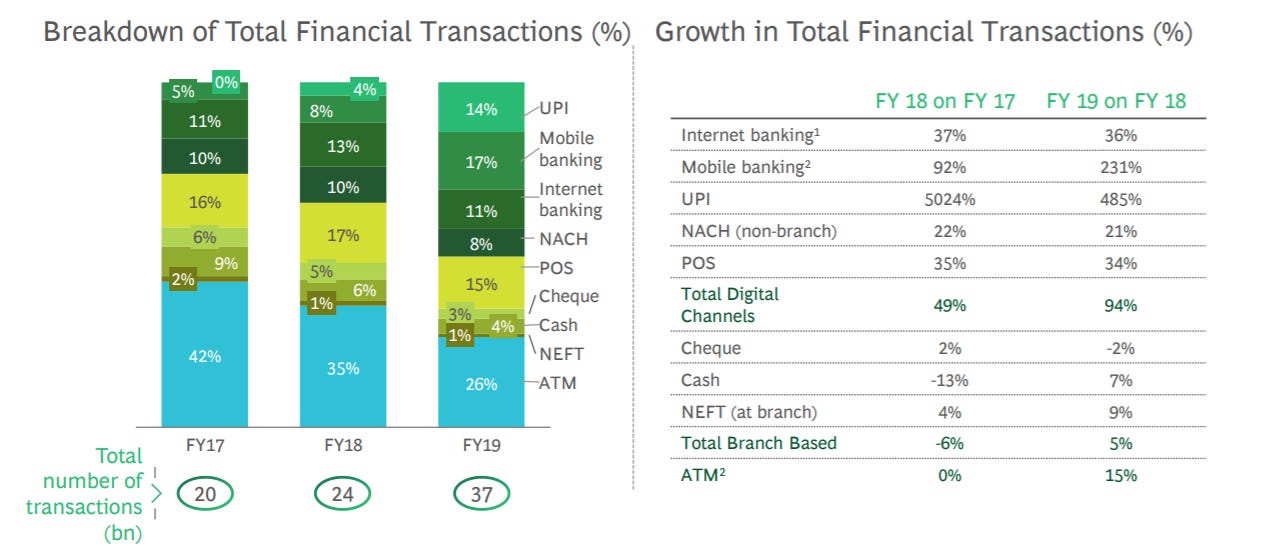

Moreover, nearly two-thirds of all transactions in the country are now digital. A detailed breakdown is below. Digital transactions have unsurprisingly spiked in the face of COVID. 1.25B UPI transactions were carried out just in the month of March, before the country shut down. Clearly, a lot of the issues that payments banks were created to solve, were solved through other means, and a banking model that aimed purely at increasing financial inclusion and digital payments ha also become somewhat besides the point.

Source: FIBAC 2019: Annual Benchmarking and Insights Report

Where and how do the neobanks play?

I think there are a few take-aways for neobanks and fintechs here.

One, there is clearly now a large financially included segment of the population to cater to. A large segment of India's population now has a bank account, but ensuring that they remain in the financial system, and move up the ladder of financial access is where the focus should now be. Creating products to cater to the very diverse financial needs of the many different Indians does create distinct business opportunities (there have been many different definitions of India 1, 2, and 3, or indeed the differences between India and Bharat; Sajith Pai's article is always useful reference). Undeniably, the business models and monetization mechanisms will be pretty distinct. A neobank catering to blue collar workers has to be a scale play, whereas one catering to urban millennials probably has a few more levers to play with in thinking of how to monetize. And yet, no matter who the neobanks cater to, there will be challenges in monetization. Recent moves to cut UPI interchange fees to zero, are just plain bad news for any fintech player in the country, and neobanks are no different. Payments and interchange are not going to be a source of revenue.

Like their American counterparts, Indian neobanks are partnering with existing banks to provide their services, which means they will face similar challenges in terms of their cost structure. After its experimentation with payments and small finance banks, the RBI is unlikely to grant new bank licenses for a few years, instead focusing on integrating the new players to the banking sector, and giving them time to stabilize and find their footing. This will impose limitations on the range of things a neobank can do (though the flipside of the argument is that it also ensures their immediate focus is on finding the right niche to play in).

Partnerships with banks are one part of the equation; neobanks are also likely to partner with providers of other financial products to offer access to investments, insurance, and even loans. Niyo, for example, already does this, offering investment products such as Mutual Funds (it has a partnership with Goalwise), digital gold, and the ability to purchase personal insurance. Given the extremely fragmented nature of India's financial landscape - with Non-Banking Finance Corporations, insurance companies, and capital market intermediaries making up other components of the financial services sector - neobanks could provide customers value in being a single point of access to a variety of financial instruments. Here an easy to use interface, and great customer experience would make an offering truly sticky, and really allow for brand recognition.

At the same time, it is important to recognize that for all the neobanks' talk of building super user friendly and customer-centric platforms, it's not like the incumbents in India have been sitting still. Many of the big banking players were slow to get on to the UPI bandwagon, much to their detriment. They have since course corrected. Ironically, the State Bank of India, the country's largest public sector bank, might be the original neobank mover in the country. It launched a fully digital offering, Yono in November 2017, and by the end of 2019 had ~17M registered users and ~6M digital savings accounts (63% of all SBI savings accounts are now opened through Yono). SBI's scale and size helps it here, and it already offers 34+ financial products including mutual funds, credit cards, and insurance on Yono. Neobanks will likely have to reconcile both competing and collaborating with their bank partners, especially when it comes to becoming the primary bank account of their customer (which is what will give them the kind of data they need to do the interesting things like smarter underwriting, etc.)

As is always the case in India, there are also things happening on the sidelines. Financial regulators last year started to work on an account aggregator framework with the aim of building data rails that allow the sharing of financial information between regulated financial institutions. Like UPI, this framework has the possibility of being a massive game changer. Having learnt from their UPI experience, the big banks are already in the process of adopting the framework. How the account aggregators shape up and how quickly they are adopted will be incredibly important in determining if India's population can go from unbanked to underbanked to being better served. But it also puts neobanks, which operate in a regulatory grey zone, at a disadvantage.

Finally, while I am all for more financial inclusion, the prospect that neobanks, if they take off, will make a complex and opaque industry even more intermediated is very real. India is still at a point where public trust in private financial institutions - or indeed private corporations of any kind - can erode very quickly. The Yes Bank saga has already done a lot of damage on this front. People depend on being able to withdraw and move the money in their bank accounts. Even a small misstep by a neobank - not unthinkable at all if you look at their experiences globally - will not bode well for any of the players in the space. Layer upon layer of complex provider agreements, that only start getting peeled apart much to the bewilderment, shock, and frustration of a customer when something goes wrong is perhaps what worries me the most about neobanks in the Indian context.

There are a lot of ifs here, but I'll end by simply saying, there is clearly a lot happening in consumer retail banking in India and some of the neobanks have really experienced founders / operators at the helm. As an observer it will be interesting to see how their products evolve and adapt and where things go.

Absolutely agree with you on most points - limited pain points to solve for Indian retail banking consumers - interest not as steep in India compared to Brazil (Nubank) or fees is not as exhorbitant as in UK/US, for any major disruption on pricing. Incumbents are moving fast to reimagine the experience they offer (and also want to see if the more established ones will even partner with such disrupters rather than upping their game). Then you also have other players like Gpay/PhonePe who are carving out smaller verticals from the Financial Services ecosystem as an offering. And then there is regulation, there is dependency which a Neobank currently can't circumvent. Will be really interesting to see how these Fintech veteran founders create a differentiated offering that can bring in sufficient sustainable revenue.

I am carrying a contrarian view on this - RBI should allow new entities of certain scale to get a banking license maybe at a short scale initially like how small finance banks are given the licences to operate with pure digital play first - with conditions such as insuring 90% of the deposits and not allowing to play much with it but isn't that already part of the game ...

US has more than 9000+ commercial banks where as India has around 60+ :)

Too much regulation and control of the state may not result into fast forward innovation in this space.