The Land of Agglomerators

Welcome to the roughly 1,000 new subscribers who joined after Vedica’s amazing two piece deep dive of Reliance. If you’re new here and want to read some of our older posts, Vedica’s piece on neobanks is a must read! And I quite enjoyed writing about ISAs in India. Today’s post is about a slightly niche topic- the venture industry in India

I recently read a great post by Nikhil Basu Trivedi on the bifurcation between Agglomerators & Specialists venture firms, and it got me thinking about the Indian venture industry. But first up, let's define what Agglomerators & Specialists are:

Agglomerators, according to Nikhil, are firms that invest across every stage, every sector and are becoming larger in size (fund size & team size). They also tend to have a dedicated team focussed on helping portfolio companies in key areas (eg: recruiting, marketing, and business development).

On the other hand, we have specialists (either by sector, stage or both). Some key characteristics of these firms are that they have smaller funds & teams, tend to be more collaborative (co-lead rounds), but their key advantage lies in being able to focus in their speciality.

If you wanted to explore the implications of Agglomerators vs. Specialists & the future of venture, do read Nikhil's piece, this piece is purely to explore the different types of firms in India.

At this point there are well over 100 venture firms in India, however there are only a handful of firms that have a sizable ownership in multiple companies that have gone onto raise significant growth rounds and/or have exited. Realistically there are only less than 25 firms that compete for ownership in the best companies, have raised multiple funds and have delivered some returns to their LPs (in alphabetical order)- 3one4 Capital, Accel Partners, Blume Ventures, Chiratae Ventures, DSG Consumer Partners, Epiq Capital, Fireside Ventures, Helion Ventures Partners, India Quotient, Inventus Capital Partners, Kae Capital, Kalaari Capital, Lightbox, Lightspeed Venture Partners, Matrix Partners India, Nexus Venture Partners, Prime Venture Partners, SAIF Partners, Saama Capital, Sequoia Capital India, Stellaris Venture Partners, VentureHighway, WaterBridge Ventures

This graph segments VC firms into agglomerators (top right quadrant) and specialists (the other three quadrants). The list of firms is by no means comprehensive.

There aren't too many firms that specialize in a particular stage or sector in India. Here are a couple:

Sector: DSG Consumer Partners & Fireside Ventures specializes in consumer brands in the early stages.

Stage: Blume Ventures, India Quotient & 3one4 Capital largely focus on the early stages (pre-seed, seed & post-seed). And A91 Partners & Epiq Capital on the later stages (both funds are fairly new)

It's also important to note that Blume, India Quotient & 3one4 have raised Opportunity Funds in the last couple of years (backing their best performing cos). As Nikhil points out specialist firms that have been successful turn to becoming agglomerate firms, since it is easier to raise larger funds. Both Blume & India Quotient could fall into this category- Blume raised their first fund in 2011 with a final close of $20M, and recently closed their third fund of $100M with a opportunity fund of $40M, along with incubating a thriving portfolio services division. Similarly, India Quotient started with a maiden fund of $4.9M and closed two funds last year (a $60M third fund & a $40M opportunity fund).

Both Blume & India Quotient seemed to have started as the founding partners institutionalizing their angel investing and while Blume & India Quotient earlier would participate or co-lead seed pre-seed & seed rounds, we now see them lead seed & pre-Series A rounds with further participation up to the B, C rounds of their leading portfolio companies. If Blume & India Quotient continue to deliver outsized returns on their funds. ShareChat & Unacademy could be fund-returners for India Quotient & Blume respectively. I think it's plausible that Blume & India Quotient start investing in A/B+ rounds by their 5th or 6th flagship fund.

And while some early stage funds are backing their existing portfolio companies throughout later rounds, other traditionally Series A+ funds are looking at seed & pre-seed companies more closely. Just in the last 2 years Sequoia, Lightspeed & Accel have launched programs to help (& in some cases fund) early stage startups in India. Sequoia seems to have the most comprehensive "product" for early stage companies (out of the three firms) with their Surge program. The firm also brought on ex-Google India head & notable angel investor, Rajan Anandan, as a Managing Director to help run & develop Surge. The program provides early stage companies in SE Asia with $1-2M in seed funding along with "company-building workshops, global immersion trips and support from a community of exceptional founders." The program been quite successful has so forth helped companies like Khatabook, Doubtnut, Classplus, Procol who have since raised additional funding and are in a growth stage.

Similarly Accel & Lightspeed have their Founder Stack & Extreme Entrepreneurs programs where they don't necessarily provide funding to the selected companies but mentor the companies and take them through programs lasting several weeks. And while Lightspeed/Accel don't take up equity stakes in these companies, when the companies are ready to raise capital they have the advantage of a pre-existing relation. It's to soon to talk about Founder Stack- the first cohort was announced a month ago, but Lightspeed invested in Yellow Messenger's Series A & B rounds (Yellow Messenger was part of EE's inaugural batch in 2018).

It's also worth noting that Sequoia and Lightspeed are somewhat different than the other Agglomerator firms on the growth side of investing. While Lightspeed India has an India fund for their early-stage & venture investments, Lightspeed also has a global growth fund that leads growth rounds in Indian companies (Udaan & Okcredit to name a few) and the firm is able to back founders through their growth journey as well. On the other hand, Sequoia is the only Agglomerator firm with a dedicated growth team & Indian growth fund and can thus back companies from the earliest stages (with Surge) to starting up towards leading their growth rounds as well. One of the advantages, as a firm, of being an agglomerator is that the firm can catch winning opportunities at different stages- if a firm missed out on a company on the seed or A, they can still lead the B if they are an agglomerator. As Nikhil points out Sequoia might already be somewhat of a Super-Agglomerator in the US and I think it's fair to say that holds in India & SEA as well- they can offer more "products" to founders aka seed, venture & growth funding along with further support in engineering, finance, legal, marketing & more through their platforms/specialists team, which certainly gives them an advantage over other funds.

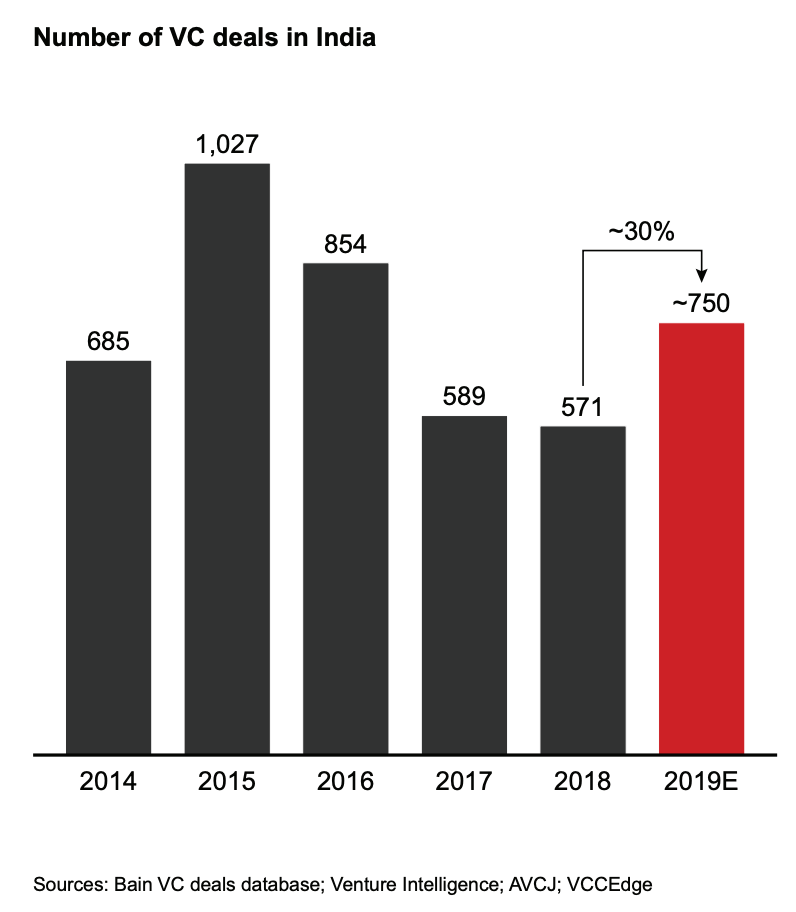

So why are almost all funds agglomerators? My guess would be that the Indian startup market isn't deep enough yet for a specialist fund from a sector perspective & the successful seed funds move up the fundraising cycle while the non-performing ones die out. Over the last 6 years, there really hasn't been a significant increase in the number of VC investments being made (~4500 deals over 6 years, averaging out to ~750/year). Meanwhile rounds are getting larger and more competitive so VCs are more incentivized to fight over the same deals (seed firms going deeper, venture firms investing earlier).

It also isn't terribly easy to raise a new fund in India, which is probably why we don't see as many investors leaving their existing funds to start new funds (partners leaving Helion to start Stellaris Venture Partners & Arkam Ventures, or leaving Sequoia to start A91 Partners are a few examples) nor do we see too many new funds being started (FirstCheque & iSeed are a few new funds started by first-time institutional investors). And the reason being that with India's startup market not deep enough, India's LP base is also not large enough. And raising a new fund from international LPs in the Indian market by a first time venture fund manager is probably close to impossible. Which is why even funds like iSeed & First Cheque are largely backed by the operator's network (other investors, founders & operators) and thus it makes sense that these are largely pre-seed/seed funds. I would imagine raising a growth focussed fund in India without prior institutional experience might be much harder- former Sequoia partners founded A91 Partners & Rishi Navani (prev. cofounder & M.D. at Matrix Partners) founded Epiq Capital.

There are a couple of sectors that are now a bit more mature & have a large number of new companies coming up where a new fund could potentially solely focus on that sector- Enterprise SaaS & FinTech to name a few. The question still remains who will start these funds. Of the top 20 funds, there are probably <100 GPs and another ~100 Principals/VPs who might have the ability to raise capital from institutional LPs for a sector-focussed fund. In the US, we've seen Founders & Operators at successful startups join the investment team of firms, but in India that isn't as common- Harsha Kumar (Ola) at Lightspeed, Amit Jain (Uber India) & Rajan Anandan (Google India) at Sequoia are an exception to this. Thus it's probably safe to assume that while a lot of Indian founders & operators angel invest heavily, they aren't as interested in formalizing & institutionalizing their practice. And even if they do, there's not too many angels who tend to in only a particular sector (Amrish Rau & Jitendra Gupta (both ex-Citrus Pay & PayU who invest in FinTech cos might be a counter-example).

And with the emergence of new funds & syndicates (iSeed, AngelListIndia, LetsVenture), angels & later stage firms investing earlier, pre-seed & seed might continue to become more & more competitive in India, following the trend in the US. It wouldn't surprise me if firms like Nexus & Matrix also start their "early stage" programs either akin to Surge or Founder Stack/Extreme Entrepreneurs as everyone wants access to the best founders and companies. I also wonder how this affects the power dynamics between investors & founders- Investors have large been in control in the last decade of Indian venture, but with an increased set of funders competing for the same companies, founders might have more options to choose from resulting in more favorable terms for them.

I do want to end on the fact that while I am a keen observer of the Indian venture space, I have not been an investor who has ever raised a fund or deployed capital, but have developed my thoughts through reading about the space and conversations with investors in the industry that I really respect.

Thanks to all the folks who read drafts of this piece for their feedback, I really appreciate it. And Vedica for her help with editing this piece.

Where would you classify hedge funds in this framework? Some of them play a key role. The most famous among hedge funds, Tiger Global, started the avalanche with Flipkart.